Summary:

The sector which once happened to be the favourite of investors, delivering double digit growth rates, today is reeling under a lot of problems. The specter of 2G scam just doesn’t seem to go away and with the way the investigations are currently going on respite seems far fledged. A KPMG survey points out that Telecom is the second most corrupt sector in the country. But does this mean that telecom is going towards being a sunset sector? Probably not; there is still a lot of penetration potential in the country. 3G is in its nascent stage. BWA is also picking up speed. The telecom ministry is set to come out with a new telecom policy this year. So the sector has a lot to look forward to.

A lot was expected from the union budget 2011; let’s see if the budget met the expectations of the sector and what impact it will have.

Key Observations:

ª The economic survey 2010 -11 termed the introduction of 3G and Broad band wireless access as the “key frontiers” of the growth of telecom sector.

ª The production of telecom equipments in value terms increased from Rs.48,800 crore during 2008-09 to Rs.51,000 crore during 2009-10.

ª Exports of telecom equipment have also increased from Rs.11,000 crore in 2008-09 to Rs.13,500 crore during 2009-10 and are expected to increase to Rs.14,000 crore in 2010-11.

ª India may have achieved a teledensity of over 65 per cent, but as many as 62,443 villages are still to get a taste of telecom revolution that started since 1995-96.

Highlights of telecom subscription data as on 31st January 2011

What the sector expected from the budget:

The growth of telecom sector has fueled the inclusive growth agenda as telecom services reach more remote parts of the nation. The government minted a lot of money from the sale of 3G and BWA license last year. Having contributed so much to the government coffers the sector did expect a lot from this year’s budget. Let’s have a look at some these expectations –

1. Tax Holidays/subsidies for expansion to remote areas:

Since the ARPU and subscriber density both are low in rural markets, rural penetration does not make a strong business case. The industry would like if the government thought about granting tax concession/ subsidies for rural expansion.

2. Rationalization of taxes:

The industry is subject to multiple levies (service tax, license charges, spectrum charges including universal service obligation fees, VAT, entry tax etc) and a significant portion of the revenue from the customer goes into the government kitty in terms of taxes and license fee through revenue share. In this scenario, a rationalization of the existing revenue sharing license fee regime is of utmost importance, which would help players by reducing administrative hassles and also allow them to maintain their effectiveness in the market. The industry has also been demanding that multiple levies should be phased out and replaced with a single levy, which can be implemented in a transparent manner.

3. Decrease import duty and taxes for broad band access:

The government should consider decreasing the import duty on broad band access devices. This will help to reduce the cost of broad band access and increase penetration. If the access points are available at low cost then the service providers can offer BB at lower cost to customers.

The government should also consider removing or reducing the service tax on BB so that its penetration can be improved.

The Budget

The government expects to raise Rs 29,648.33 crore (Rs 296.48 billion) through recurring licence fees and other usage charges from the telecom sector, according to the general budget for 2011-12 tabled by Finance Minister Pranab Mukherjee on 28th Feb.

The usage charges include licence fees from the telecom operators, receipts on account of spectrum usage charges and auction of third generation (3G) and broadband wireless access (BWA) spectrum.

As per the last budget, the government estimated accruals worth Rs 49,799.55 crore by auctioning spectrum for 3G and BWA access services. But it ended up raking a bounty of Rs 1.08 lakh crore through these auctions in 2010-11.

While the revenue from the auction of 3G spectrum stood at Rs 65,000 crore as against the expected Rs.35,000 crore, the BWA spectrum fetched the government over Rs 38,000 crore.

Key points from the budget

ª Full exemption from basic customs duty and CVD to components for manufacture of battery chargers. Components of Hands-free headphones of mobile handsets including cellular phones are also fully exempt from customs duty and CVD. The validity of the exemption from special additional duty on mobile phones is being extended till March 31, 2011.This will make the mobile phones cheaper.

ª The Minimum Alternate Tax (MAT) has been increased from 18% to 18.55. This will adversely affect the telecom companies.

ª The reduction in the surcharge on corporate tax from 7.5% to 5%

Reaction of the Industry

The budget did not bring a smile on the faces of the industry with many calling it a big letdown.

"We in the cellular industry are deeply disappointed that the industry that has provided so much to national development and has made India the second largest and fastest growing telecom market in the world, has not received the encouragement and nurture befitting such an important engine of economic development and nation building," said Rajan Mathews , director general, Cellular Operators Association of India.

S.C. Khanna, general secretary, Association of Unified Telecom Service Providers of India, said that though village broadband has been taken into consideration there has been no tax benefit for the sector.

The budget failed to address the concerns of the industry. No Tax breaks were announced for rural services were announced. The MAT was increased by half a percentage. Overall the reaction is that the sector has been overlooked by the finance minister.

No announcement was made to clear the ambiguity surrounding corporate tax treatment on spectrum charges and the associated borrowing costs. Similarly nothing was said on tax holidays for consolidation.

The year ahead

2011 is set to be the year when the telecom ministry comes out with a new telecom policy, ‘new telecom policy 2011’. The last time the policy was amended was in 1999. Since then a lot has changed in the sector, intense competition, advent of 3G technology, BWA. All this demands a fresh look at the policy used to govern the sector. The new policy is welcome news. But it is to be seen exactly how things unfold.

The government has indicated that it intends to increase the current preferential treatment of “Made in India” telecom equipments in the new telecom policy. This move is set to meet strong opposition by telecom lobbies COAI and AUSPI.

The JPC set up by the government will investigate the allocation and pricing of licenses and spectrum from 1998 to 2009. The JPC is expected to submit its report in the next three months.

The government might be on the lookout to auction the 700 MHz spectrum for BWA.

Facts and Figures

Service provider wise market share as on 31.01.2011

Bharti Airtel continues to be the number one in subscriber figures; crossing 200 million subscriber mark in Q3, followed by Reliance and Vodafone. Mobile number Portability has not turned out to be a game changer as some had predicted. The market leaders haven’t lost much of their base due to MNP.

Service provider’s share in net additions during the month of January 2011

Performance of Industry Players

Let us have a look at the financial performance of Bharti Airtel, Idea and Reliance communications. We are considering the financial year 2010-11.

Figures are in millions of rupees.

EBITDA figures

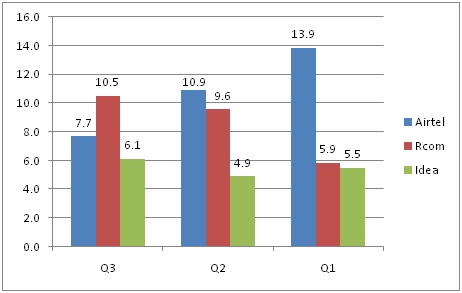

EBITDA for Airtel has seen a good rise from Q1 to Q3 whereas it has been quite stable for both Rcom and Idea.

EBITDA margin

Figures in percentages

Net Profit Margin

No comments:

Post a Comment